Introduction

In the fast-moving world of small and medium-sized businesses (SMBs), finance teams are under pressure to drive efficiency, accuracy, and compliance, all while doing more with less. With the adoption of financial process automation tools rising sharply, 55% of SMBs “strongly agree” automation is essential to business efficiency. SMB Group+1

But automation isn’t simply a plug-and-play fix: without a strong governance framework around it, automation can introduce new risks (errors, fraud, compliance gaps). This article explores how SMBs can build governance around finance automation, focusing on roles, logs, and evidence, to ensure control, transparency, and trust.

The Need for Governance in Finance Automation

Why SMBs are automating

- According to the 2024 SMB Group research, SMBs increasingly view automation as critical: 55% strongly agree it enhances business efficiency, and 35% somewhat agree. SMB Group+1

- Automation shifts finance teams from mechanistic tasks (data entry, reconciliation) to decision-support, forecasting, and strategic input. NetSuite

- SMBs face macro headwinds (inflation, supply-chain, cybersecurity threats) and look to automation to bolster resilience. SMB Group

The risk side: Why governance matters

Automating finance workflows can deliver big upside but if not governed properly, you risk:

- Untracked changes, invisible errors, or process drift

- Compliance issues (especially where audit/log-evidence is required)

- Weak controls (lack of segregation of duties, no audit trail)

- Data integrity problems: “garbage in = garbage out”. Paro Finance Solutions+1

In short: Automation doesn’t remove the need for internal controls, it transforms them.

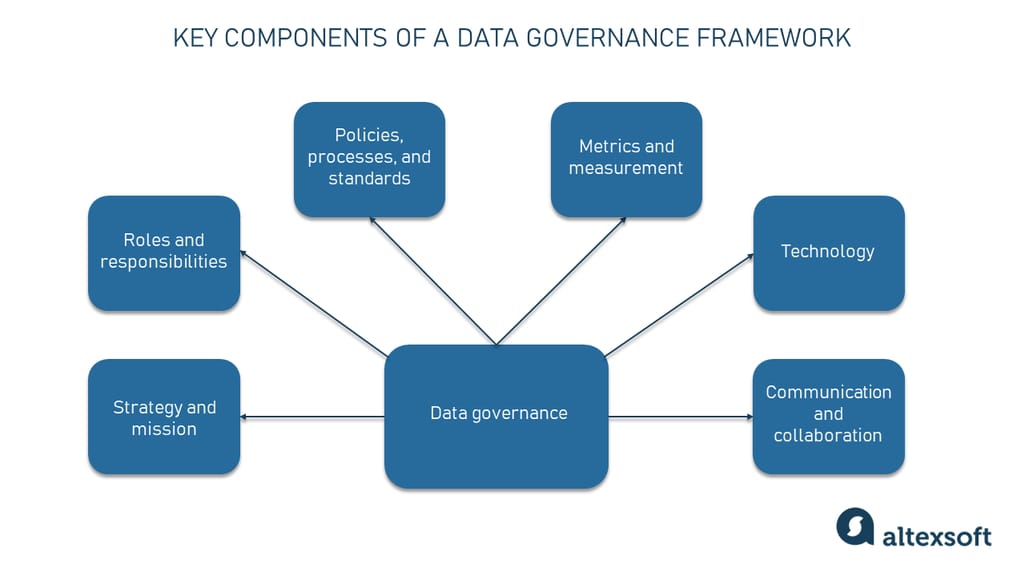

Key Governance Pillars: Roles, Logs & Evidence

Governance of finance automation can be viewed via three inter-related pillars:

1. Roles & Responsibilities

Defining clear roles ensures accountability and prevents overlap or ambiguity. Some key roles for an SMB finance automation governance model:

- Finance Automation Owner: Typically someone in the finance function (e.g., Senior Finance Manager or Controller). Responsible for the automated processes: design, performance, compliance.

- Process-Subject‐Matter Expert (SME): Finance or accounting team member with deep process knowledge (e.g., month-end close, accounts payable).

- IT/Automation Lead: Responsible for the technical implementation of automation tools (RPA, workflow automation, bot-engines).

- Internal Controls / Compliance Lead: Ensures that automation is aligned with internal controls, audit requirements, compliance standards (e.g., SOX-style, local statutory).

- Data Owner / Steward: Ensures the data inputs feeding the automation are accurate, consistent, and high quality.

- Audit / Logging Lead: Responsible for making sure logs are maintained, tamper-resistant, and accessible for review.

For SMBs, many of these roles may be combined (due to resource constraints), but the key is to assign responsibility and avoid all tasks falling on a single individual. Good governance means role clarity. According to Paro’s best practice guide: “defined processes and stakeholders” are fundamental for finance/data governance. Paro Finance Solutions

Real-world scenario

A mid-sized manufacturing SMB introduces automation for invoice processing. The Finance Automation Owner sets up the workflow, the SME verifies business rules (e.g., invoice threshold, approval hierarchy), IT/Automation Lead implements the bot, and the Compliance Lead monitors for segregation of duties. If one person tries both approving and executing the invoice process, the control risk rises.

2. Logs & Audit Trails

Logs capture what happened, when, and by whom. They form the backbone of accountability in an automation-governed finance environment.

Why logs are critical

- They provide traceability and root-cause analysis (if something goes wrong).

- They support internal and external audits.

- They demonstrate control over automated processes (who did what, when).

- They help detect anomalies, unauthorized access, or process deviation.

What logs should include

- Timestamp of each automated action (e.g., bot executed payment, data entry performed).

- User-ID or system identity that triggered the action (whether human or bot).

- Input data snapshot / version (so you can see what data the automation consumed).

- Outcome/result of the action (success/failure; exception).

- Change history (if someone modified the workflow or parameters).

- Exception or error logs (and resolution workflow).

- Retention metadata (how long logs will be stored and archived).

In advanced scenarios, you might also include tamper-proofing mechanisms (e.g., using blockchain or append-only logs) to strengthen trust. arXiv

Real-world scenario

An SMB rolls out an automated month-end close process. Every time the bot runs a reconciliation script, the log captures: “19-Oct-2025 21:15 – BotID: FINBOT01, Reconciliation run for Ledger A – All variances < 0.02% – duration 3 m45s”. Later, the controller spots a variance spike; the logs enable them to trace back to “19-Oct-2025 19:45 – Manual data import by User: John_Smith – Data file older version” and correct the root cause.

3. Evidence & Review

Governance isn’t just about running processes—it’s about verifying them. Evidence is the proof that automation is working correctly, controls are functioning, and compliance is maintained.

What constitutes evidence

- Periodic control-self-assessment results (e.g., the automation ran as expected, no control failures).

- Audit reports (internal or external) verifying automation controls and outcomes.

- Metrics and KPIs: e.g., number of automatic exceptions, processing time improvement, error rate reduction.

- Documentation of process changes (workflow versioning, approvals for changes).

- Training records for roles interacting with automation (ensuring human-in-the-loop remains knowledgeable).

- Exception logs with resolution evidence.

- Access review results (who has rights to bot management, who changed workflows).

Review cadence & governance meetings

- Monthly operational review by the Finance Automation Owner and Process SME.

- Quarterly control review by the Compliance Lead (including log review, exception trends).

- Annual audit of the automation framework (roles, logs, evidence) and governance effectiveness.

- Change-management board (any major automation change needs documented request, approval, testing, go-live sign-off).

Real-world scenario

The CFO of an SMB receives a quarterly dashboard: “Invoices processed via automation: 3,452. Exceptions flagged: 28 (0.8%). Average processing time: 45 minutes vs 2 hours last quarter.” The dashboard also highlights that access rights were reviewed on 10 Oct 2025 and no unauthorized changes found.

Building Your SMB Finance Automation Governance Program

Here is a practical roadmap tailored for SMBs.

Step 1: Define scope and processes for automation

- Map the finance processes you intend to automate (accounts payable, month-end close, cash reconciliation, forecasting).

- Identify risks in each process (error, fraud, inefficiency).

- Prioritise automation opportunities with proper governance built-in.

Step 2: Design governance structure around roles, logs and evidence

- Assign roles (as outlined above) and document responsibilities.

- Define what logs will be captured, how, by whom, and their retention.

- Define what evidence will be collected, who reviews it, and how often.

- Develop a governance policy document (even a one-pager) summarising the above.

Step 3: Implement automation with built-in governance

- Choose a finance automation tool that supports logging, user identity, versioning and audit-trail capabilities.

- Build dashboards for real-time monitoring of automation metrics.

- Configure alerts for exceptions, unusual volumes, rule changes.

- Make sure that data quality (input data) is governed via a Data Owner/Steward.

Step 4: Monitor, review, adjust

- Use logs to review exceptions, trends and process drift.

- Conduct periodic governance reviews (roles still correct? Segregation of duties maintained?).

- Collect evidence and present to stakeholders (Finance, Audit, Leadership).

- Adjust policies, controls, roles as the automation footprint grows.

Step 5: Document change, management & audit readiness

- Any change to the automation workflow (e.g., a new business rule, a bot upgrade) should follow a change-request process: request → review → test → approve → go-live → log change.

- Ensure audit-readiness: logs, evidence and governance documentation should be organised and retained so external/internal audits can be satisfied.

The Pay-Off: Benefits for SMBs

- Greater transparency into finance operations (you know who did what, when).

- Stronger controls with automation that is not “black-box”.

- Enhanced compliance readiness (audit trails, evidence, defined roles).

- Reduced risk of manual error, fraud, process drift.

- Improved efficiency and freed-up finance resources to focus on value-add activities.

- Better decision-making, thanks to clean data, consistent processes and reliable automation.

Why It Matters Now

- With the volume of finance data increasing and automation accelerating, poor governance means poor outcomes. Safebooks+1

- For SMBs, regulations and stakeholder expectations (investors, lenders, auditors) are raising the bar: you need to show you are in control.

- Automation without governance is like a fast car with no brakes.

- Investing in governance pays off: being able to scale automation confidently and mitigate the hidden risks.

Conclusion

For SMBs implementing finance automation, governance around roles, logs, and evidence isn’t optional, it’s foundational. By clearly defining who does what, capturing what happens (and when), and proving that controls are working, you build trust, control, and resilience. Automation becomes not just a productivity tool, but a governed, auditable, scalable asset.

If you’re ready to take your finance automation to the next level, while staying in control, governance is your launch pad.

Leave a Reply