Introduction

In today’s fast-changing business environment, fraud and especially payment fraud and check-fraud, remains a major exposure for organisations of all sizes. When approvals and payments follow manual, fragmented workflows, fraudsters find easier opportunities (whether internal or external).

A powerful mitigation strategy is the use of automated approvals: workflows, checks, controls and validations built into an automated system (rather than purely manual processes). These automated approvals bring greater visibility, enforce stronger controls, and reduce the “fraud window”.

In this article we’ll explore:

- The key problems and pain-points in manual approval/payment workflows.

- How automated approvals reduce fraud exposure (including check fraud).

- Real-world scenarios and best practices for PeopleOps / finance / back-office teams.

- How PeopleOps can lead the change, coordinate with finance and tech, and continuously monitor the results.

The problem: manual approvals + payments = fraud risk

Before diving into the solution, it helps to understand why manual workflows create fraud vulnerabilities.

Fragmented workflows, human error & lack of visibility

- With manual approvals, invoices or payment requests often pass through several people (requestor → approver → payment-team) and often rely on email, spreadsheets, paper checks or loosely connected systems. This leads to weak audit trails and higher error/fraud risk.

- According to one source, when organisations retain manual (or semi-manual) credit/approval workflows, “manual credit approvals increase the chargeback rate significantly compared to automated processes”. Resolve Pay

- Manual AP / payment workflows make it harder to enforce segregation of duties (i.e., no single person should approve and pay out) and harder to guarantee role-based access, document matching, duplicate detection. Corcentric+1

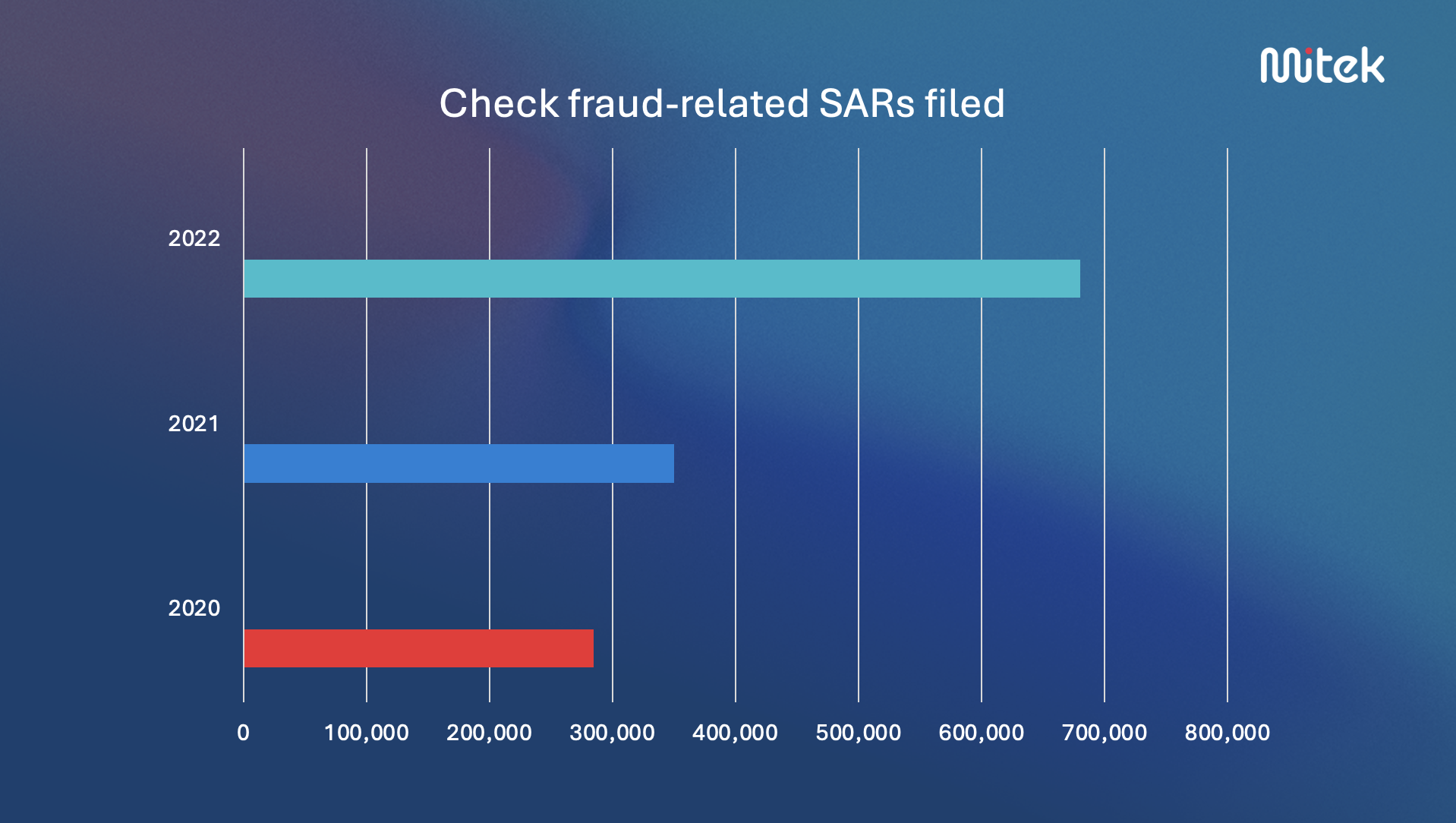

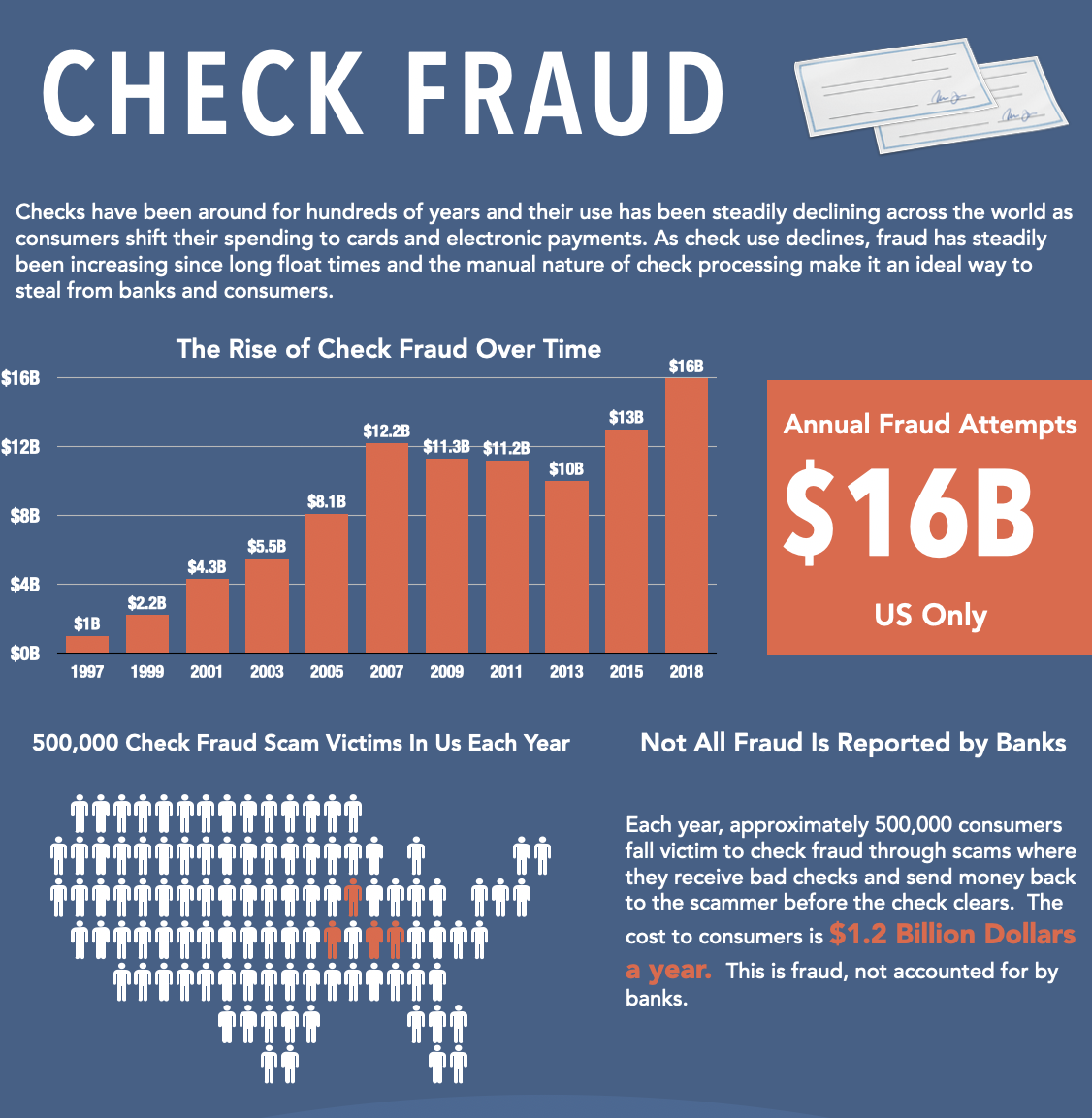

- Check-fraud remains a big issue: for example, one blog cited “checks continue to be the payment method most vulnerable to fraud, with 65% of respondents reporting they had faced this type of fraud attack in 2023.” cloudxdpo.com

Hidden fraud-paths: vendor fraud, duplicate payments, forged checks

- Vendor collusion: fake vendors, fictitious invoices, inflated amounts. If approvals are weak, blank checks or forged invoices may slip through. docuphase.com+1

- Check-fraud: Paper checks can be altered, stolen, or diverted. When control is weak, fraudsters intercept checks or run off-system duplicates. The automated payment/digital approach helps here. docuphase.com+1

- Duplicate payments or unauthorized changes (for instance, vendor bank account changed without oversight) become easier to execute when controls are manual and distributed. Tax1099+1

Business & PeopleOps pain points

From a PeopleOps / back-office perspective, the impacts include:

- Loss of trust and reputation (internal workforce, auditors, finance teams).

- Time wasted in exception investigations, reconciliations, audits.

- The need for enhanced controls that may slow processes and frustrate business units.

- Over-reliance on key individuals (single-person approvals) which is risky when they leave or are absent.

- Difficulty scaling processes when the business grows or becomes more complex (global vendors, remote teams, digital payments).

Automated approvals: the fraud-reduction benefits

Introducing automated approvals into your workflow can substantially reduce fraud and check-fraud exposure. Here’s how, with the mechanics and controls explained.

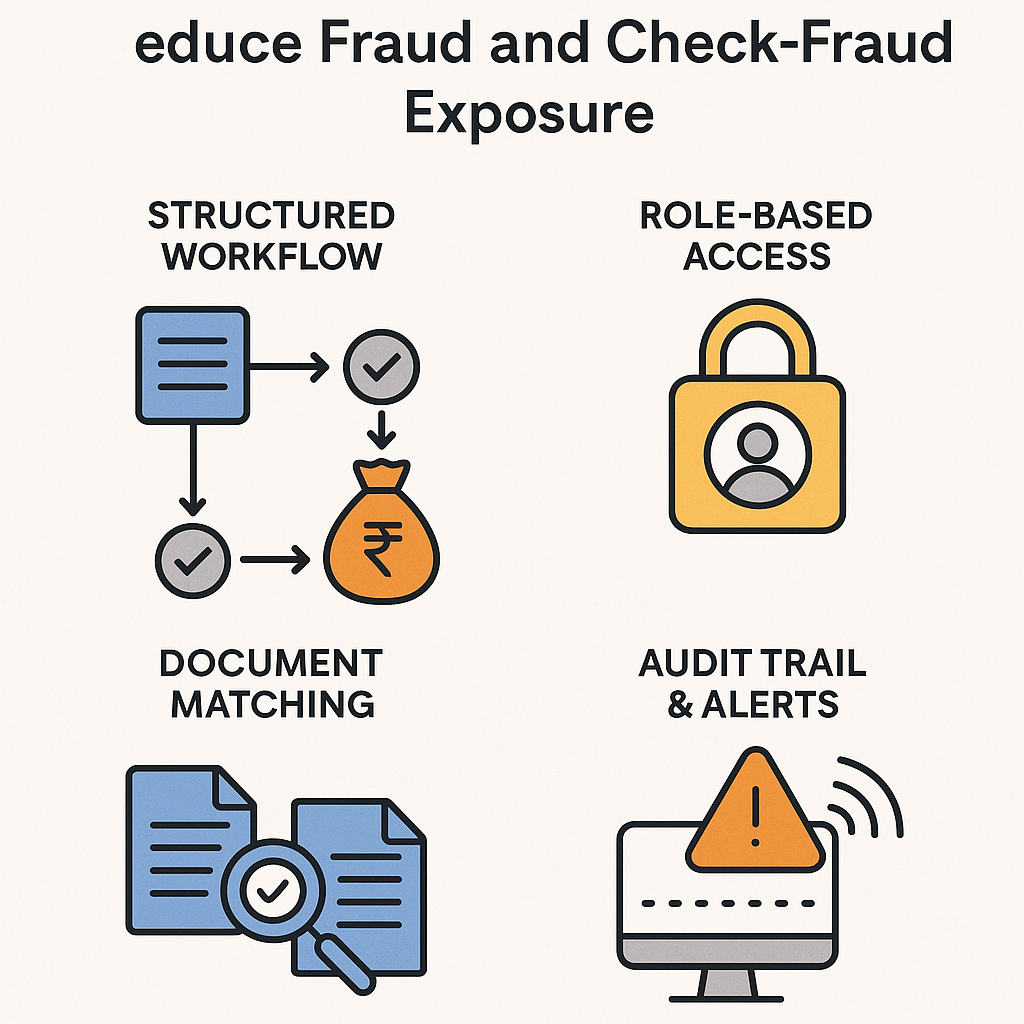

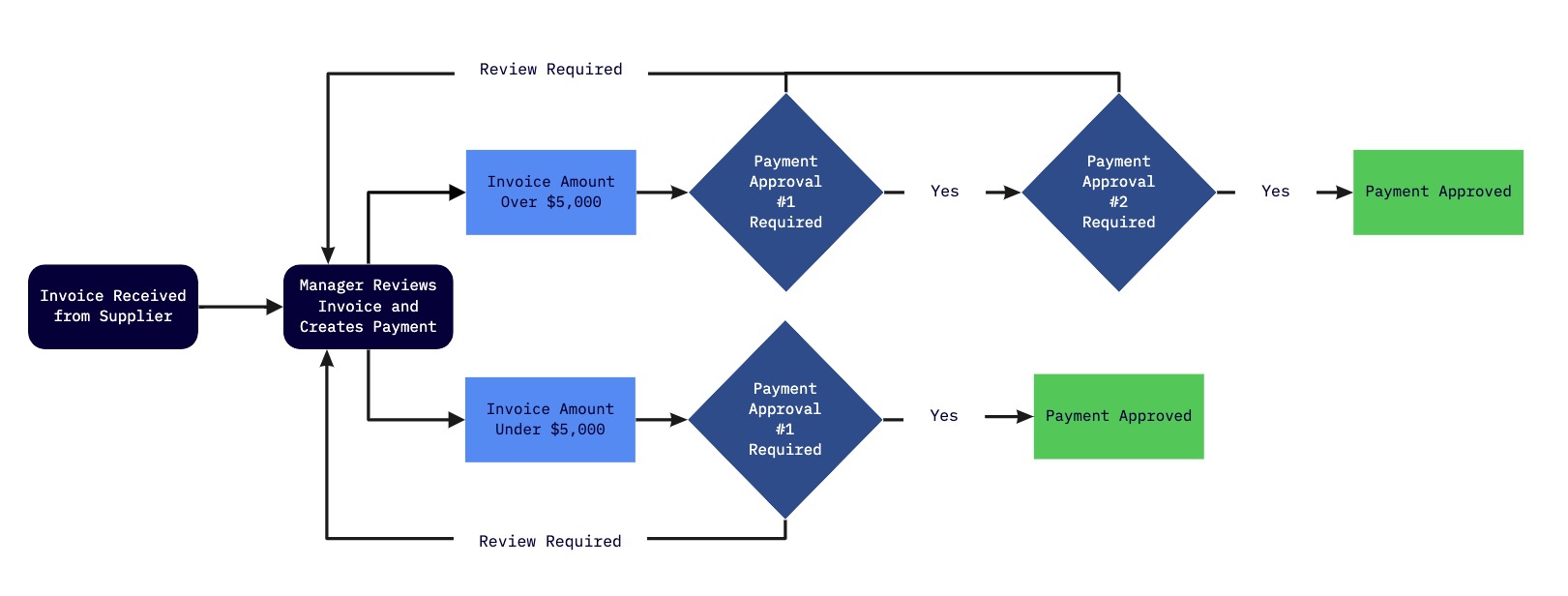

1. Enforcing structured workflow & segregation of duties

Automated approval systems can define and enforce approval chains: e.g., invoice → first-level approver → second-level approver (if amount > threshold) → payment team.

- This ensures that one person cannot both approve and pay, reducing internal fraud risk. Corcentric+1

- System-based routing means no bypassing of approvals, no “my email got lost” excuses, and every step is recorded.

2. Role-based access & permission controls

Automated tools allow teams to assign specific permissions: e.g., who can create vendor records, who can approve bills, who can change bank details.

- This limits exposure: “only authorised users handle sensitive AP information.” Tax1099+1

- Reduces risk of fraud through improper access or account takeovers.

3. Document matching, vendor verification, duplicate detection

- Automated systems can automatically check invoices against purchase orders, contract terms, vendor master lists. This helps detect anomalies or fraud. Quadient+1

- Duplicate payment detection: automation flags repeated invoices or vendors, reducing overpayment risk. cloudxdpo.com+1

- Vendor verification: validate vendor bank account details, tax IDs, banking status before payment. Tax1099

4. Audit trail, visibility and real-time alerts

- When approvals are automated, every action (who approved, when, what amount, what vendor) is logged. This transparency serves both operational oversight and audit/compliance. docuphase.com+1

- Real-time alerts/rules: if a payment request falls outside norms (unusual vendor, new bank account, high amount) the system triggers alerts or even blocks until review. This reduces the window for fraud. cloudxdpo.com+1

5. Shift from checks/paper to digital payments and workflows

- Automated workflows often tie into digital payments (ACH, electronic transfers) rather than paper checks. Checks are inherently more vulnerable to fraud (alteration, interception) and automation reduces check-fraud risk. Tax1099+1

- Digital payments come with encryption, validation, and easier traceability.

6. Efficient review allows focus on exceptions rather than mass manual checks

- With automated approvals, teams spend less time on every invoice manually, and more time on “exceptions” or flagged items. This means they can focus resources where risk is highest rather than spread thin.

- In one case study, moving from manual to automated screening enabled earlier detection of fraudulent account applications at scale. services.mjvinnovation.com

Real-world scenario: check fraud and how automated approvals help

Let’s walk through a typical scenario in a mid-sized company, and how automated approvals change the story.

Scenario (Manual Process – High Risk):

– Company X receives an invoice from “Vendor ABC Supplies” for ₹ 2,50,000.

– The invoice is sent via email to an approver, who manually checks it, then forwards to finance for payment.

– Finance issues a paper check for the amount, mails it. Meanwhile, vendor bank details were recently changed but no separate verification happened.

– A fraudster intercepts the check or uses forged vendor details, cashes it, the payment shows cleared in the ledger but finance only realises weeks later when reconciling.

– Loss: ₹ 2,50,000 + audit/investigation cost + reputation hit.

With Automated Approvals & Controls:

– Company X uses an AP workflow tool. Invoice is submitted and automatically matched with PO/contract. Vendor bank details change triggers system-verified check (vendor bank account must be validated).

– Approval workflow: amount > ₹ 1,00,000 triggers second-level approval. A new vendor/fresh bank details triggers real-time alert.

– Payment via electronic transfer; paper check option disabled for that vendor. The entire process is logged (time-stamps, approver IDs).

– Because of the controls, the fraudulent change in bank details is flagged and held for manual review. Fraud prevented.

Outcomes:

– Risk of check-fraud (via paper check interception) eliminated.

– Stronger vendor validation blocks fake vendor or fraudulent banking changes.

– The audit trail means if something does go wrong, it’s easier to investigate and trace.

– Control burden on staff is lower (they are focusing on exceptions) rather than manually verifying every step.

Role of PeopleOps (and cross-functional teams)

From the PeopleOps perspective, automated approvals have more than just cost/fraud benefits, they support organisational health, governance and culture.

Facilitating cross-team alignment

- PeopleOps should partner with Finance, IT, and Security to design and implement automated workflows. It’s not just a finance project, when approvals affect spend, vendor onboarding, and controls, multiple stakeholders must be aligned.

- Define clear roles and responsibilities: who initiates requests, who approves, who monitors. This ties back into segregation of duties.

Training & change-management

- Automation introduces new behaviours: staff need to understand how new workflows work, what triggers alerts, how to handle exceptions, how to interpret dashboards/logs.

- PeopleOps can lead training, reinforce policies (e.g., vendor changes must go via system, no bank-details changes via email).

- Culture of “we trust the system” rather than manual override: When employees bypass the tool, you lose the benefit of automated controls.

Monitoring and metrics

- PeopleOps and Finance should agree on KPIs: e.g., number of invoices processed via automated workflow, number of flagged payments before/after, time to approval, fraud incidents prevented, number of check payments vs digital payments.

- Regular review: Are the rules working? Are false positives too high (frustrating business units)? Are controls overly rigid? Automation must adapt.

- Continuous improvement: Update approval thresholds, rules, vendor verification logic as business changes.

Implementation best practices & things to watch

Here are several best practices and caution points to maximise benefit and minimise risk of automated approval adoption.

Best practices

- Define clear rules up-front: approval thresholds, vendor change triggers, bank detail change audits, segmentation based on amount, region, vendor risk.

- Use role-based access controls (RBAC): ensure only authorised roles do certain tasks. Tax1099+1

- Vendor master-data hygiene: keep vendor records up-to-date, de-duplicate vendors, verify bank account changes.

- Switch to electronic/digital payments where possible: reduce exposure to check fraud. docuphase.com

- Audit logs and dashboards: ensure every step in approval/payment process is logged, searchable, and visible.

- Exception‐handling process: Not everything can or should be fully automated, build clear paths for flagged items, manual review, escalations.

Things to watch / risks

- False positives / too many alerts: If automation produces many alerts that turn out to be non‐issues, it burdens staff and reduces trust. As research shows, balance between alerting and business flow is key. arXiv

- Over‐rigid rules leading to delay: If every small invoice triggers multiple approvals, business units might bypass the system or revert to manual ‘work-arounds’.

- Change management resistance: People comfortable with manual approvals may resist new systems unless there is buy-in and training.

- Technology / integration risk: The automated workflow tool must integrate with vendor/payment systems, ERP, accounting software. Gaps reduce benefit. Tax1099

- Evolving fraud tactics: Automation is powerful, but fraudsters adapt. Systems need to update rules, use anomaly detection, monitor emerging threats. Wikipedia

Conclusion

In summary, automated approvals are a critical lever for reducing fraud and check-fraud exposure. For organisations aiming to strengthen their back-office controls, ensure governance, and scale operations safely, automation is no longer optional. From a PeopleOps standpoint, this transformation touches people, process, policy and culture not just technology.

By implementing structured workflows, role-based access, vendor/bank validations, digital payments and real-time visibility, business leaders can reduce fraud risk, enhance efficiency and provide stronger audit trails. Meanwhile, PeopleOps can act as the glue: coordinating across functions, training staff, monitoring metrics and ensuring the system works for both business needs and security demands.

If you’re ready to take the next step, consider a pilot project: choose a high-volume, moderate-risk approval workflow (e.g., vendor payments below ₹ 5 lakh), implement an automated approval tool, compare before/after metrics (approval times, flagged items, manual exceptions, noted fraud attempts), and expand from there.

Automation doesn’t eliminate fraud entirely but it shifts the odds in your favour significantly, while also supporting business agility and operational scalability.

Leave a Reply