In today’s rapidly evolving business-environment, small and mid-sized businesses (SMBs) face a pivotal decision when designing their finance technology stack: do you build, buy, or integrate? Each path has its advantages and trade‐offs. For finance and PeopleOps leaders, the stakes are high; the wrong decision can lead to excessive costs, slowed growth, or failures in compliance and scaling.

In this article, geared for both technical and business readers in the PeopleOps domain, we’ll walk through:

- What each approach means in the context of an SMB finance stack

- The key pain‐points and problems we see in practice

- How to evaluate which option fits your business

- Real-world scenarios where each makes sense

- How PeopleOps can help steer the decision and execution

1. Why the decision matters for finance stacks in SMBs

The state of play

SMBs are under increasing pressure to modernize their finance functions. Several trends amplify this:

- Growing demands for real‐time financial visibility, forecasting and automation of manual tasks, especially as teams move beyond spreadsheets.

- Cloud, SaaS, and embedded finance options are now accessible to smaller organizations, turning what was once enterprise‐only into viable choices.

- Especially in PeopleOps, finance technology intersects with payroll, HRIS, expense management, and data integrations. So your finance stack isn’t isolated, it must play nicely with broader PeopleOps systems.

- SMBs often have constrained resources (budget, engineering, IT support) relative to large enterprises. So decisions around cost, time to value, risk and maintenance are more acute.

- The “build vs buy vs integrate” question isn’t just theoretical; it influences how fast you can scale, how agile you are, and whether you’re investing in your core competency or diverting away.

The consequences of a poor decision

Choose the wrong approach and you might face:

- Long time to market: Building internally could take far longer than planned. Open Ledger+1

- Hidden costs: Even when buying or integrating, implementation, customization and maintenance add up. Formstack+1

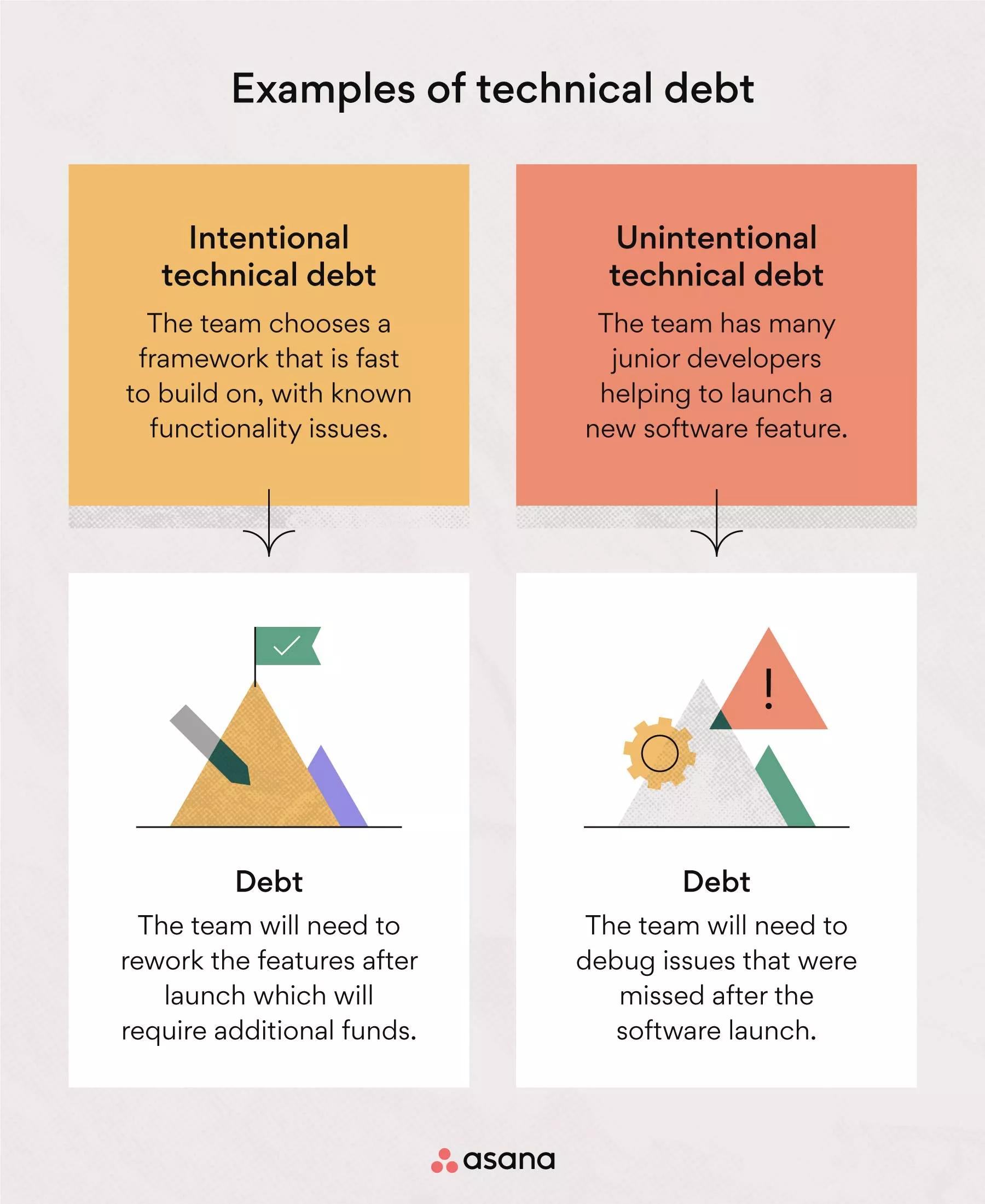

- Technical debt and maintenance burden: A custom build may look appealing, but then you own all the upkeep, updates, security patches. Medium

- Mis-alignment with business needs: If you build something too bespoke, you risk having a system that’s difficult to update, integrate or adapt.

- Lost focus: Engineering time spent building non-core finance functionality may distract from strategic initiatives.

2. Defining Build, Buy, and Integrate in the SMB Finance Context

Build

This means your organization (or a contractor you hire) develops the finance software/infrastructure in‐house. For example: you build a custom accounting ledger, a unique budgeting/forecasting tool, or tailor‐made expense reimbursement system.

Pros:

- High customisation: The system is tailored exactly to your workflows and business model.

- Full control: You own the code, data models, UI/UX, and aren’t bound by vendor lock-in (if managed well).

- Potentially unique advantage: If your finance process is a true differentiator, building can support your strategic edge.

Cons (especially for SMBs):

- Time to value: Building takes longer than buying a ready system. nCino+1

- Resource & skill demands: Requires developer/IT skill, ongoing maintenance, upgrades, documentation.

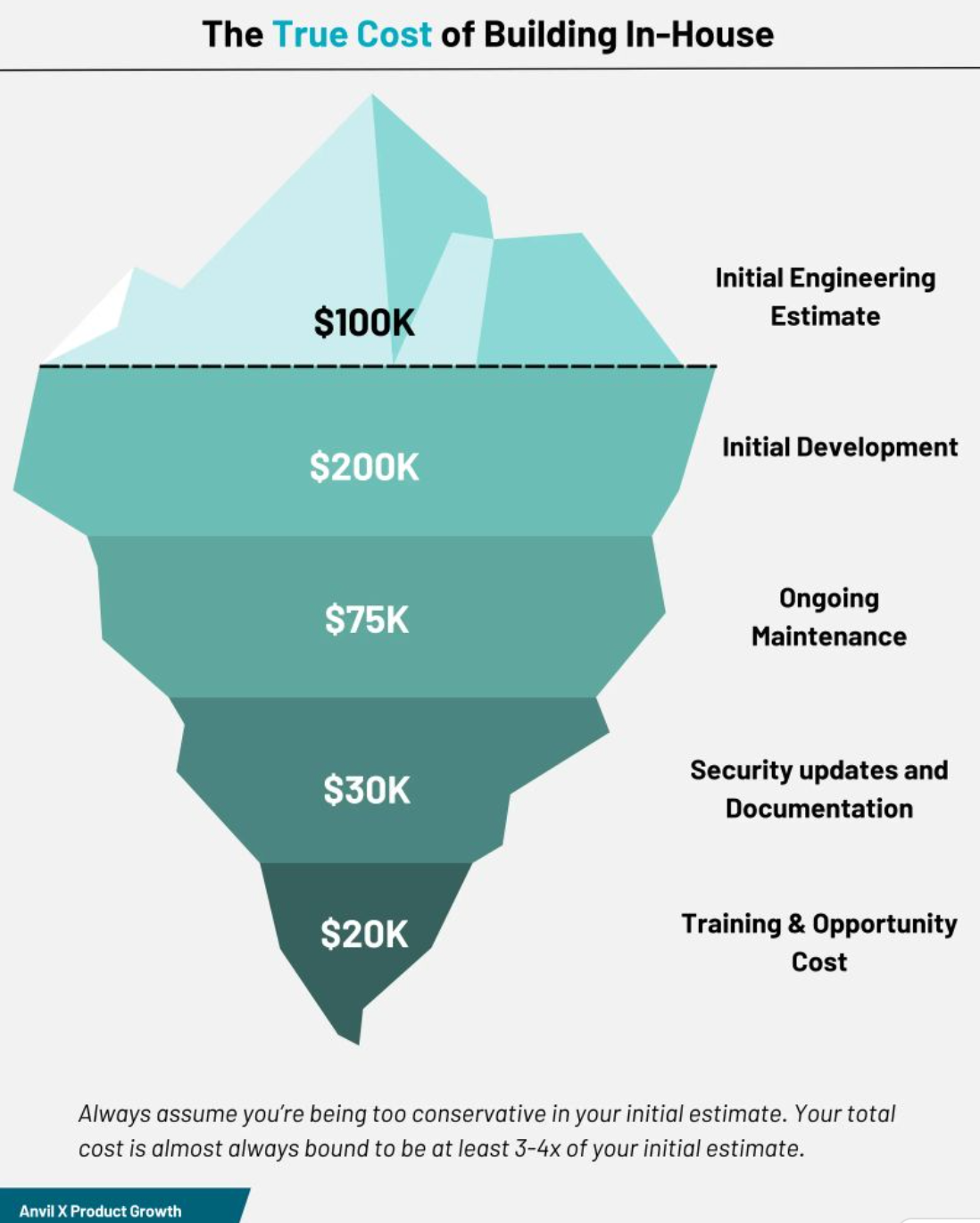

- Hidden long-term cost: Maintenance, updates, scaling, security, compliance. Example: one organisation found building a custom accounting module cost vastly more than integrating. Open Ledger

- Risk of failure: Scope creep, unexpected complexity, missing integrations. dispatch.me

Buy

You purchase a commercial, off-the-shelf (COTS) solution (SaaS or on-prem) for your finance stack. For example: subscribing to a cloud accounting platform, budgeting/FP&A tool, or expense management system.

Pros:

- Rapid deployment: Vendor solution means faster time to go-live.

- Continuous updates: Vendor handles upgrades, new features, security. LiquidX+1

- Lower upfront risk: Many vendors have proven scalability and reliability, and you don’t need to build from scratch.

- Potential cost savings: Avoid full build costs and maintenance burdens.

Cons:

- Less customization: You might need to adapt workflows to the vendor’s model (or pay for advanced customisation).

- Vendor dependency: You rely on the vendor’s roadmap, pricing, support, integration capabilities.

- Fit‐gap: Some unique or highly specific processes may not be well supported.

- Integration burden: Even a bought solution may need significant integrations with your HRIS, CRM, analytics stack, etc.

Integrate

Often a hybrid or middle path: you buy foundational modules and then integrate them (via APIs, connectors, middleware) with other systems, or build small custom extensions on top of a core platform. In some usage “integrate” might also mean using a best‐of‐breed network of point tools that are stitched together.

Pros:

- Balanced flexibility & speed: You leverage vendor solutions for core functionality and customise only what you need.

- Scalability with control: You can pick best-in-class tools and integrate them, rather than one monolithic system.

- Lower build cost: Compared with full build, build/integrate hybrid abstracts some of the heavy lifting. For example, SMBs using low-code platforms have seen faster time to value. StartupTalky

- Future-proofing: Modular integrations allow you to swap out components as needs evolve.

Cons:

- Integration complexity: Managing data flows, mapping, APIs, security and versioning can be challenging.

- Governance overhead: You must ensure the integrated stack is coherent, maintainable and monitored.

- Incremental costs: While less than full build, you still pay for vendor subscriptions + integration/maintenance.

- Potential for “tool sprawl”: With many point tools, you may lose coherence or get weaker user experience if not managed.

3. Key Pain‐Points SMBs Face in Finance Tech Stacks

From our experience in PeopleOps and finance tech advisory, several recurring pain-points come up:

Manual processes & lack of automation

Many SMBs still rely on spreadsheets, manual data entry, delayed reporting, or disconnected systems. This results in:

- Errors and rework

- Delayed decision making

- Limited scalability

Disconnected systems and data silos

Finance intersects with HR, payroll, CRM, billing, analytics. If these tools don’t integrate, you get:

- Duplicate data entry

- Inconsistent figures (e.g., HR headcount vs cost analytics vs budget)

- Loss of visibility across functions

Suboptimal time to value

When finance teams implement new tools, they often underestimate how long implementation will take, how much customisation is required, and how much change management is needed. The result: long deployment, user fatigue, low adoption.

Resource constraints

SMBs typically have smaller IT or dev teams. They may lack internal expertise to build custom systems or to integrate many vendor tools. Also budget is more constrained, so ROI must be clear.

Technical debt and maintenance

Whether you build or integrate, long-term maintenance is often underestimated. Updates, monitoring, user support, training, data migrations, all add to cost and complexity. Medium+1

Changing business models and scaling

As SMBs grow (new geographies, new products, new regulatory regimes), finance stacks need to adapt. Legacy builds may not scale. Vendor tools may not support unique workflows. The “future-proofing” question becomes real.

Compliance, security, and risk

Finance systems handle critical data. Whether you build or buy, you must ensure data security, audit trail, GDPR/other regulation compliance. Vendors may give assurance, but integration still introduces risk.

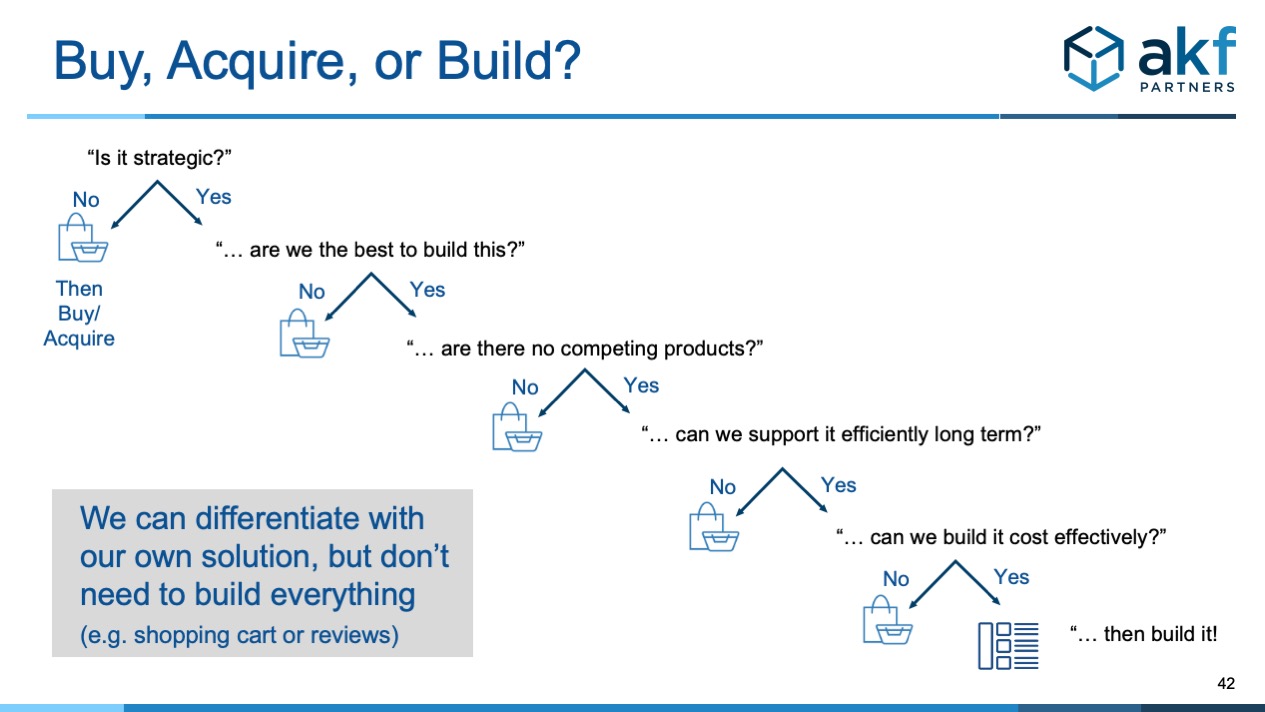

4. Framework for Choosing: Build vs Buy vs Integrate

Here’s a practical framework to help PeopleOps/finance leaders evaluate which approach is best for their SMB.

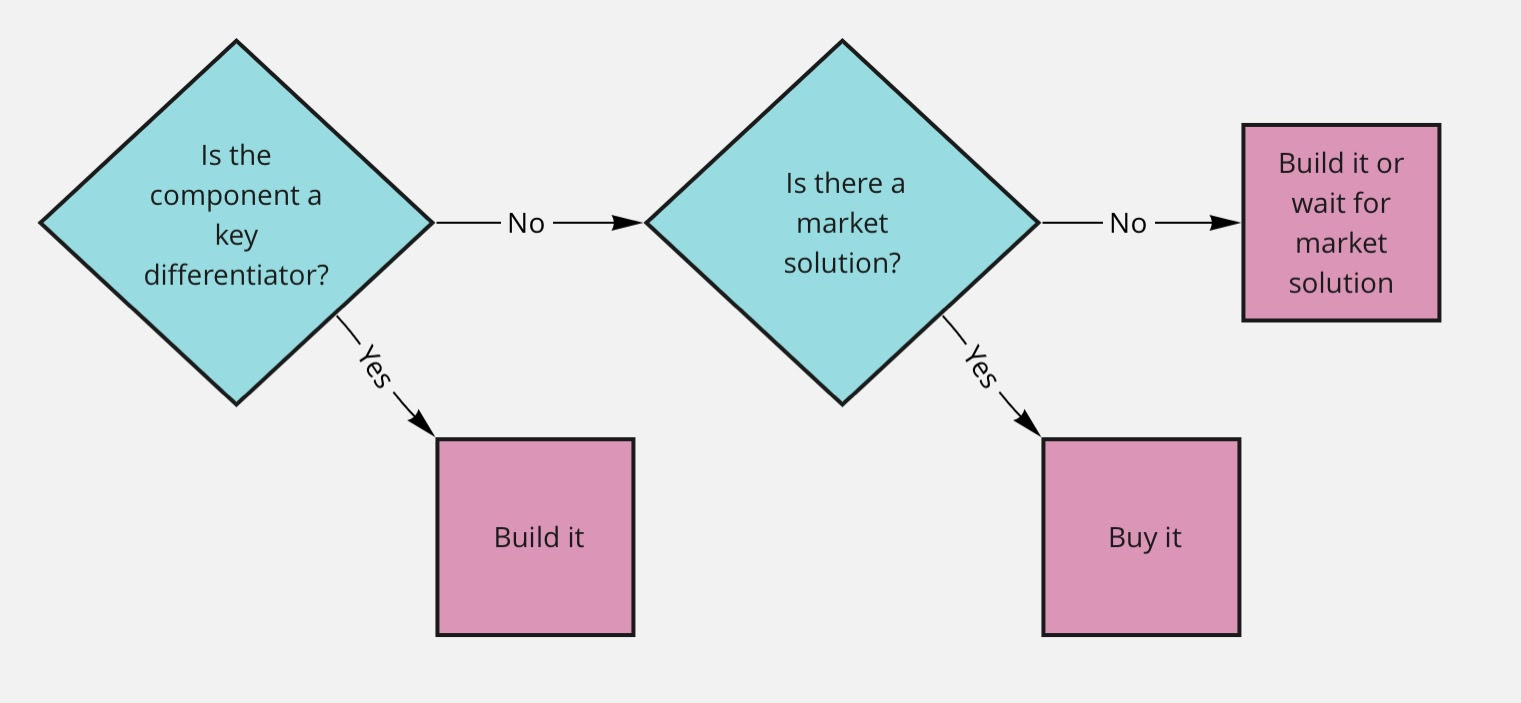

Step 1: Define your core differentiated finance capabilities

- Ask: Which parts of our finance stack really drive our business value or competitive advantage? If it’s a standard commodity function (e.g., general ledger, accounts payables, standard budgeting), buying may suffice.

- If you have unique workflows, special accounting rules, a novel business model requiring bespoke logic, you might need build or heavily customised integration.

- As one product‐leader put it: “Start by asking: what makes our product uniquely valuable to customers? Everything else is a candidate for buying.” Medium

Step 2: Assess time to value and resources

- How fast do you need this functionality? If you need something quickly (quarterly board cycle, audit deadline, scaling event), buying or integrating is often faster.

- What internal resources do you have (developers, IT ops, integrations expertise)? Without this, a build can be a risk.

- Consider opportunity cost: what will your engineering/finance team not do if they are busy building this? Margin Makers by Zip

Step 3: Total cost of ownership (TCO) and risk

- For build: estimate initial development cost + ongoing maintenance + upgrades + staff/change management. Example: one SMB build of accounting module showed huge cost over 6 years compared to integration. Open Ledger

- For buy: include license/subscription cost + implementation/customisation + vendor lock‐in risk + integration cost.

- For integrate: ticket cost + subscription + integration/maintenance overhead.

- Also evaluate risks: technology debt, vendor roadmap, security/compliance gaps, data migration issues. dispatch.me

Step 4: Integration & scalability considerations

- How well will your chosen solution integrate with existing systems (HRIS, CRM, billing, analytics)?

- Will it scale as your business grows (new markets, more transactions, more users)?

- Does the vendor support your future needs, or will you be constrained?

- Are there pre-built connectors or APIs that simplify integration? Or will you need heavy custom development?

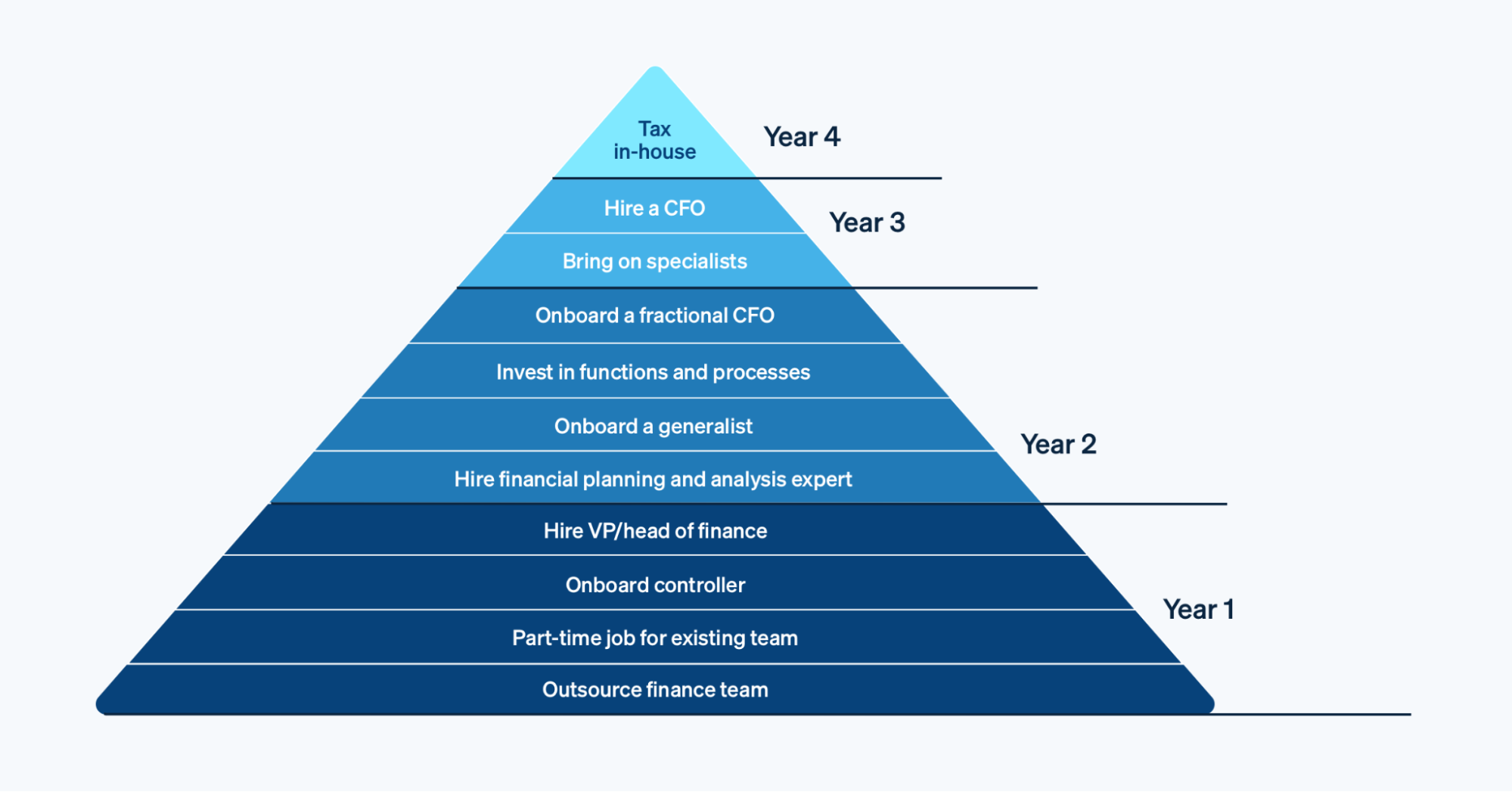

Step 5: Decide hybrid/hybrid approach (“buy foundations, build advantage”)

- Many experts now advocate for a hybrid approach: buy core modules (ledger, AP/AR, budgeting) and build or integrate only the parts that reflect your unique differentiator. nCino

- This gives you the best of both speed and tailored differentiation.

Step 6: Change management & adoption

- Whatever path you choose, ensure you plan for user adoption: training, process redesign, data migration, ongoing support.

- PeopleOps plays a critical role here: aligning stakeholders (finance, IT, HR), communication, governance, training.

5. Real‐World SMB Scenarios

Scenario A: Early-stage SaaS startup – chooses Buy

A SaaS startup with ~50 employees and limited engineering set wants to move from spreadsheets to a scalable budget/forecasting tool. They don’t yet have unique finance workflows and speed is essential. They select a commercial SaaS budgeting & forecasting platform, implement within 6 weeks, leverage pre-built templates, focus engineering efforts instead on product features.

- Outcome: Faster time to value, minimal custom build, cost predictable.

- Trade-off: Some workflows are adjusted to fit the vendor model.

Scenario B: Mid-sized services SMB with unique billing model, chooses Build/Integrate Hybrid

A services company (~200 employees) has a complex billing model (based on milestones + usage + variable staff rates) which off-the-shelf tools don’t support out‐of‐the‐box. They buy a core finance platform (general ledger, AP/AR) and then build a custom billing engine that integrates via API into the core. Data from billing flows into finance, HR, and project management systems.

- Outcome: Retain unique billing advantage, maintain standard finance foundation.

- Trade-off: Need for integration expertise and ongoing maintenance of the custom part.

Scenario C: Established SMB in manufacturing, considers Build (but ultimately shifts to Integrate)

A manufacturing SMB with ~500 employees has legacy systems and believes it needs to build a custom finance and ERP module that reflects their workflows (multi‐site, multiple currencies, unique inventory costing). They start building but after 12 months realise cost overruns, delays, and integration headaches. They pivot to buying a best-of‐breed finance/ERP core and integrating modules, completing implementation in the next 6 months.

- Lesson: Build route may look appealing, but hidden costs/time make buy+integrate more practical.

- Real world evidence: “While building is often more time-consuming whereas buying leads to rapid market entry and response.” nCino+1

6. How PeopleOps Can Enable the Decision & Implementation

As a PeopleOps professional, you play a strategic role in this process. Here’s how you can add value:

Align business & technical stakeholders

- Facilitate conversations between finance leadership, IT/dev teams, HR/PeopleOps, procurement.

- Define business requirements (finance, PeopleOps, HR), workflows, pain‐points, success metrics.

- Translate between business language (“faster month-end close”, “better headcount visibility”) and technical language (integration points, APIs, maintenance burden, user adoption).

Own change management & adoption

- Ensure training programs, user onboarding, documentation are built into project plan.

- Monitor adoption metrics post-go-live (are finance users using the tool, data quality improved, time saved?).

- Manage roles & responsibilities (who owns the tool, who maintains it, how will upgrades/changes happen).

Manage process & vendor/partner relationships

- When buying or integrating, help with vendor selection: evaluate vendor roadmap, integration ecosystem, data security, total cost of ownership (TCO).

- For build/integrate, ensure governance: code ownership, maintenance plan, documentation, support handoff, technical debt visibility.

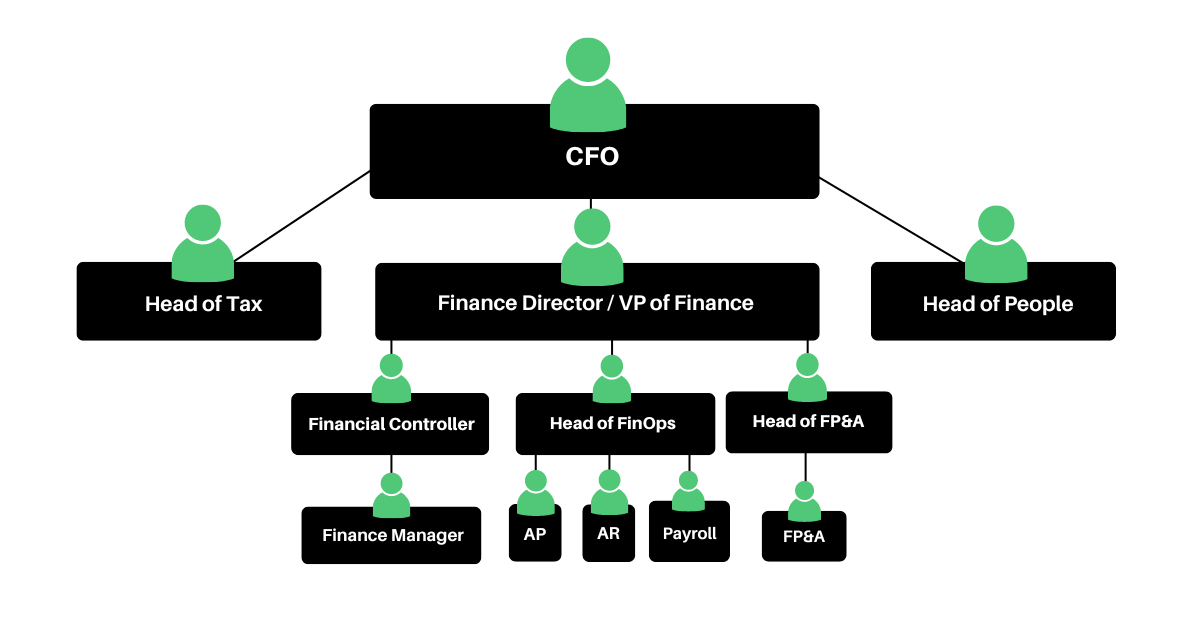

- Align finance goals with PeopleOps goals: e.g., payroll/HR/finance integration for headcount/cost visibility, role cost analytics, aligning PeopleOps metrics with finance data.

Monitor and iterate

- Finance stacks evolve. As your company grows, new needs will surface (multi-entity consolidation, multi-currency, analytics, AI/automation).

- Set up regular reviews: Is the solution still meeting needs? Are there bottlenecks? Does integration still hold? Are maintenance costs ballooning?

- PeopleOps can own the continuous improvement loop, not just the initial implementation.

7. Summary & Recommendation

In sum:

- There is no one-size-fits-all: Build, Buy or Integrate each have valid use cases.

- For SMBs with limited resources, buying or integrating tends to be more pragmatic for standard finance processes.

- Build makes sense when you have unique finance workflows that are core to your business model, and you have the resources (time, talent, budget) to support it.

- Integrate (hybrid) often offers the best of both worlds: buy the foundation, build/customise for differentiators.

- The key success factors: clear definition of what is core/unique, realistic assessment of time/resources/costs, integration and scalability planning, and governance & adoption focus.

- PeopleOps plays a pivotal role in aligning stakeholders, managing change, and ensuring the finance stack supports the broader people-and-business operational strategy.

Recommendation for PeopleOps leaders & SMB finance teams:

- Map your current finance stack: what works, what doesn’t, what are the pain points?

- List your “must-have” workflows and identify which are standard vs unique.

- Estimate your time-to-value, resource availability, and cost for build vs buy vs integrate.

- Identify vendor solutions and integration options; conduct a TCO/risk analysis.

- Choose the route that balances speed, cost, flexibility and alignment to business strategy and ensure you have the PeopleOps/finance-team governance and change-management plan in place.

Leave a Reply